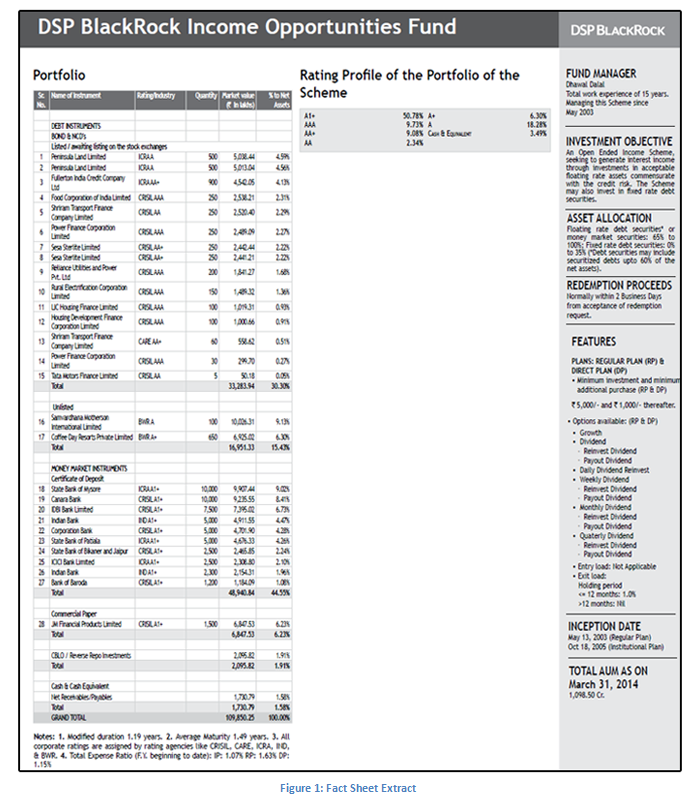

In our previous article we had discussed how to effectively study the key information elements presented in the factsheet for equity funds. In this article, we will discuss to effectively evaluate the information in a debt fund factsheet. For our discussion, we will use the March 2014 factsheet of the DSP BlackRock to evaluate, as an example, the DSP BlackRock Income Opportunities Fund from the DSP BlackRock stable. Below is an extract from the factsheet.

What are the important information elements in the fund factsheet?

Investment Objective:

As discussed in the previous article, the investment objective articulates what the fund manager intends to achieve. Debt funds aim to generate income over short term, medium or long term by investing in a portfolio of fixed income securities. In the case of the DSP BlackRock Income Opportunities Fund, the investment objective says, "An Open Ended Income Scheme, seeking to generate interest income through investments in acceptable floating rate assets commensurate with the credit risk. The Scheme may also invest in fixed rate debt securities". Therefore we can infer that, this fund is an income fund that generates income by taking acceptable levels of credit risk. Since the fund plans to invest primarily in floating rate securities, investors can expect the interest rate risk of the fund to low. To get a sense of the risk, investors should check the SEBI colour code of risk for this fund. SEBI has three colour codes for risk. Blue signifies low risk, yellow medium risk and brown high risk. The fact sheet contains the colour codes for each scheme. The colour code of the DSP BlackRock Income Opportunities Fund is blue, signifying low risk (please see below).Fund Manager Information:

Like equity funds, investors should know which fund manager is managing their funds. They should look at other schemes managed by the fund manager and the performance of the schemes managed by him. The monthly factsheet has the details of all the schemes managed by the fund house, and so the investor can find out the information regarding all the schemes managed by the fund manager. In the case of the DSP BlackRock Income Opportunities Fund, the fund manager is Dhawal Dalal. The other debt schemes managed by Dhawal Dalal include DSP BlackRock MIP Fund, DSP BlackRock Short Term Fund, DSP BlackRock Strategic Bond Fund, DSP BlackRock Bond Fund, DSP BlackRock Government Securities Fund etc. Investors should look at the performance of the other funds managed by the fund manager. We will discuss how to study performance of a fund later in the article. It is also generally believed that, longer the time, a good fund manager manages a fund, better is the potential of the fund generating higher returnsCredit Rating:

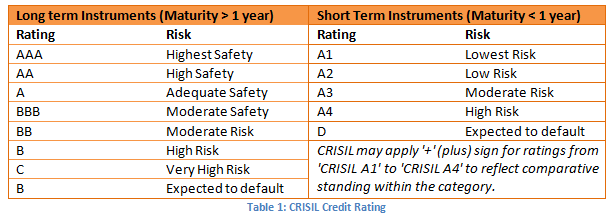

The fact sheet contains the credit ratings of the fixed income securities in the fund portfolio. Higher the credit rating, lower the yield but the risk is also lower. Usually debt fund managers in India invest in high quality securities, i.e. in securities, that are highly rated. Let us understand how credit rating scale works. The table below describes the credit rating scale used by CRISIL to rate debt securities.Average Maturity:

Investor's should also look at the average maturity of the portfolio. Average portfolio maturity on a standalone basis, is not of much significance. Investors should look at the trajectory of the average portfolio maturity over several months. If the average maturity of the portfolio is increasing, this implies that the fund manager expects interest rates to decline in the future. Interest rates have an inverse relationship with bond prices and the portfolio returns. If the average maturity of the portfolio is increasing, investors can expect the NAV of the fund to increase and vice versa. The average portfolio maturity of the DSP BlackRock Income Opportunities Fund in March is 1.49 years (see the bottom of the fact sheet in Figure 1). The average portfolio maturities for February, January, December and November are 1.36, 1.41, 1.29 and 1.17 years respectively as per the DSP BlackRock factsheets for January, December and November. Please see the chart below, for the average maturity profile of the fund.Asset Allocation:

Like for equity funds, investors should also pay importance to asset allocation of the fund. In the case of the DSP BlackRock Income Opportunities Fund, about 65% is allocated to floating rate fixed income securities and 35% to fixed rate fixed income securities (refer to right hand side of Figure 1). Fixed rate securities give greater returns when interest rates are falling, and floating rate securities give greater returns when interest rates are rising. Since we are currently in a high interest rate environment, greater allocation to floating rate securities would have resulted in higher yields for the fund. In practise, due to the absence of floating rate instruments, the fund manager has invested in money market instruments like commercial papers and certificate of deposits (see the lower left side of the factsheet in figure 1). About 51% of the fund portfolio is invested in money market securities. Money market instruments have lower maturities. Over the past few months, the money market instruments had high yields due to the high interest rate regime (see our article, Liquid Funds: A good option to park your surplus cash Part 1). Further, many income funds like, Monthly Income Plans invest a portion of the portfolio in equities. Investors in monthly income plans should regularly check the percentage of assets allocated to equities to understand the level of risk the fund manager is taking. Higher risk may generate higher returns, but the investor needs to feel comfortable that the risk level of his or her investment is in line with his or her risk tolerance. Investors should therefore pay careful attention to asset allocation.Fund Performance:

Strong performers aim to outperform the benchmark and generate good returns across all time scales. The fund should outperform the bond markets, both in a rising interest rate regime, as well as a declining interest rate regime. The fund fact sheet contains the performance of the fund versus the market benchmark on an annual (financial year) basis and since inception of the fund. Let us look at the performance of the DSP BlackRock Income Opportunities Fund, over various time periods on an annual basis, in the factsheet extract below. The factsheet also shows the growth of standard Rs 10,000 invested in the fund since inception, versus various market benchmarks. Please see the factsheet extract below, for the performance of the fund versus the market benchmark.Expense Ratio:

Like equity funds, investors should also pay particular attention to expense ratios. A high expense ratio implies a more expensive the fund. Expense ratio of debt funds is generally lower than equity funds. Investors should pay attention to the expense ratio of the fund versus its peer group. Higher expense ratio will eat into the returns of the investor. Refer to fund factsheet in figure 1. The expense ratio of the DSP BlackRock Income Opportunities Fund is 1.6% (see the bottom of the fact sheet in Figure 1). As assets under management of the fund increase, the expense ratio should go down. While high expense ratio impacts the final returns of the investor, what ultimately matters to the investor is the return on investment. Therefore, while expense ratio is important, investors should always evaluate it in conjunction with returns.

Let us look at the credit rating profile of the securities in the portfolio of DSP BlackRock Income Opportunities Fund in fact sheet extract (Figure 1).

We can see that more than 75% of the portfolio is in highly safe (low risk) securities (AA and above). A rating of AA denotes high safety and AAA highest safety, for long term instruments as per the CRISIL credit rating scale. The A1+ credit rating denotes lowest risk for short term instruments as per the CRISIL credit rating scale. This shows that the credit rating profile of the portfolio is very good and the principal risk in the fund is very low. This re-affirms the blue colour code for this fund.

It is clear that the average maturity is increasing over the last few months (except in February) and therefore the fund manager believes that interest rates will decline in the future. The investor should validate the fund manager's outlook by looking at maturity profiles of peer funds and the industry view on interest rates in general.

The fund has outperformed the market indices over most time periods. The fund factsheet also shows the growth of a standard investment of Rs 10,000/- since inception of the fund. Retail investors should note that returns above are for the institutional plans. Institutional plans have a lower expense ratio compared to retail plans. Therefore the actual returns for retail investors will be slightly lower than what is showed in the factsheet. Retail investors should adjust these returns by the difference between the expense ratio of retail and institutional plans.

Conclusion

Mutual fund factsheets contains a wealth of information that helps the investors in making an informed decision whether to invest in a fund, stay invested or redeem their units, as the case may be. If you follow a systematic approach in reviewing the fund factsheet, as described in this article, you can cull out the most important data points from the fact sheets in order to make effective investment decisions.

Top 10 Tax Saving Mutual Funds to invest in India for 2016

Best 10 ELSS Mutual Funds in india for 2016

1. BNP Paribas Long Term Equity Fund

2. Axis Tax Saver Fund

3. Franklin India TaxShield

4. ICICI Prudential Long Term Equity Fund

5. IDFC Tax Advantage (ELSS) Fund

6. Birla Sun Life Tax Relief 96

7. DSP BlackRock Tax Saver Fund

8. Reliance Tax Saver (ELSS) Fund

9. Religare Tax Plan

10. Birla Sun Life Tax Plan

Invest in Best Performing 2016 Tax Saver Mutual Funds Online

For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call

---------------------------------------------

Leave your comment with mail ID and we will answer them

OR

You can write to us at

PrajnaCapital [at] Gmail [dot] Com

OR

Leave a missed Call on 94 8300 8300

-----------------------------------------------