In our weekly call last week, we discussed our debt strategy post budget. As a part of the strategy, we discussed about the investment opportunities in arbitrage funds and recommended three funds. This week, we'll take a look at arbitrage funds, their strategy, whether they will suit you and our brief on three such funds.

What they are

Arbitrage funds take controlled exposure to equities. What do we mean by controlled exposure? They will simply carry out strategies which would have offsetting positions on various markets at the same time. In other words, the schemes take hedged positions that make them 'market neutral' or with no specific equity risk.

Arbitrage funds are open-ended equity schemes that will generate income through arbitrage opportunities arising out of mispricing across spot, futures and options market, leading to profits. They will also seek to invest some proportion in debt when warranted.

Such funds could take positions in stocks in the cash market (say buy) and an opposite position (sell) in the same stock in the derivatives market and vice versa. Similar strategy can be adopted on the index as well. These positions can be either squared off before expiry or rolled over.

Typically, volatile markets offer more arbitrage opportunities between the cash and derivative market. In the event of no adequate arbitrage opportunities, funds may choose to increase exposure to short-term debt and liquid instruments.

In all, this class of funds seek to provide you with money market plus returns. That they are treated as equity funds and hence, provide capital gains tax exemption if held for over a year makes them tax efficient short-to-medium term options. Being equity funds, they do not also suffer any dividend distribution tax.

Suitability

The first qualification to invest in these funds is that you understand how they work. Why is this so important? For two reasons: one, if you are looking for substitutes for debt funds these really are not debt funds although their risk profile may mimic low-risk debt.

Two, if you understood these funds as being equity funds, then you may wonder why they deliver low returns, when equity funds manage higher returns.

Hence, it is important to understand that arbitrage funds primarily use hedging strategies. In the process, if they generate some profit as a result of mis-pricing, you benefit more. Else you benefit about the same as you would with liquid or ultra short-term funds.

Besides understanding the thesis behind these funds, if you are looking at a time frame of 1-2 years and are primarily looking for tax efficient ways to invest in low-risk options, arbitrage funds can work for you.

Here are the funds we chose in this category:

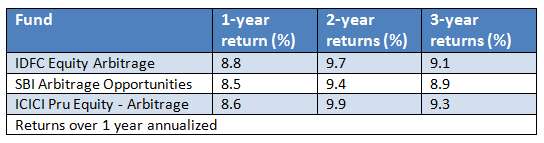

SBI Arbitrage Opportunities – Of our picks, this fund would fare as our relatively low risk pick. The fund's deviation from mean returns is very low. As of June 2014, well over a third of its assets were in commercial papers and fixed deposits; perhaps an indication that arbitrage opportunities were not high then. Still, a combination of hedging and debt holding has helped the fund deliver 8.5% absolute returns in just 6 months now.

The fund had close to 10% of its hedged equity assets in midcap stocks. This segment could possibly provide more mis-priced opportunities. Banks, cement and cement products and pharma were among the top sector exposures.

IDFC Arbitrage Fund – This fund would fare next in terms of low standard deviation and risk. At present it has about 70% of hedged exposure to equities and the rest in debt instruments – mostly certificates of deposits and other liquid instruments.

On a daily rolling return basis over the last 3 years, the fund generated an average 1-year return of 8.8%, while the maximum returns it managed over the same period was 9.7%. The sectors in which it has maximum hedged equity exposure include banks, pharma, cement, and oil and gas; weights being highest to the first-mentioned sector. The fund is also amongst the more consistent player in terms of beating the CRISIL Liquid fund Index over 70% of the times on a rolling – return basis.

ICICI Pru Equity – Arbitrage Fund– This fund seeks to hold anywhere between 65-80% in hedged equities; it can hold unhedged equity of not more than 5% and is allowed to hold the rest in debt. The unhedged position is meant to allow liquidity instead of disturbing hedged positions. Still, to the extent of such position, its risk element is slightly enhanced. This is reflected in its higher standard deviation.

That said, the maximum one year returns it generated (in the last 3 years) is also higher than the above funds at 11.2%.

Best Tax Saver Mutual Funds or ELSS Mutual Funds for 2015

1.ICICI Prudential Tax Plan

2.Reliance Tax Saver (ELSS) Fund

3.HDFC TaxSaver

4.DSP BlackRock Tax Saver Fund

5.Religare Tax Plan

6.Franklin India TaxShield

7.Canara Robeco Equity Tax Saver

8.IDFC Tax Advantage (ELSS) Fund

9.Axis Tax Saver Fund

10.BNP Paribas Long Term Equity Fund

You can invest Rs 1,50,000 and Save Tax under Section 80C by investing in Mutual Funds

Invest in Tax Saver Mutual Funds Online -

For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call

---------------------------------------------

Leave your comment with mail ID and we will answer them

OR

You can write to us at

PrajnaCapital [at] Gmail [dot] Com

OR

Leave a missed Call on 94 8300 8300

---------------------------------------------

Invest Mutual Funds Online

Download Mutual Fund Application Forms from all AMCs