Are you a salaried person!! if yes, than you must be holding an Employee Provident Fund (EPF) Account with the EPFO. It is mandatory to own a EPF account if you are in job and draws a salary of up to Rs.15,000 per month. EPF is optional for individuals drawing salary more than Rs.15,000 per month.

The EPF is maintained solely by the Employees Provident Fund Organization of India (EPFO) and any organization employing more than 20 persons is necessarily required to get registered with the EPFO.

FAQs on Employee Provident Fund

Q. Is Contribution to Employee Provident Fund Mandatory?

Yes, contributing to EPF is mandatory for the employees who have a basic salary plus dearness allowance is up to Rs.15,000 (earlier it was Rs.6,500). And those who are earning above Rs.15,000 may contribute voluntarily.

But the decision to opt out of scheme should be taken at the start of your career. In case, you have been a member of EPFO once, then you are not allowed to opt out of the scheme.

Further, opting out of the scheme will increase your in hand salary and thus your tax outgo will also increase, so it is strongly recommended to avail this scheme as this is the easiest way to build a huge corpus for retirement.

Q. What are the Tax-Benefits of EPF contribution?

Another benefit of this robust scheme is that the contribution made towards EPF is an eligible deduction under section 80C. The maximum deductible contribution is ceiling the limit of section 80C i.e. Rs.1.50 lakh for current financial year 2015-16.

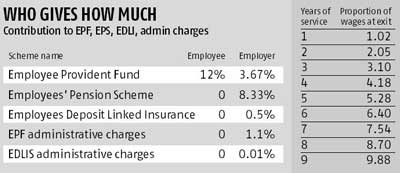

Q. What is the Break-up of EPF Contribution?

As per EPF Act, 1952, the monthly contribution of employee and employer would be divided in the following way:

So if your basic salary plus dearness allowance is Rs.15,000 than the contribution would be proportioned in the following way:

| Scheme | Employee Contribution | Employer Contribution |

| Employee Provident Fund | Rs.1,800 | Rs.550.5 |

| Employees' Pension Scheme | 0 | Rs.1,249.5 |

| Employee Deposit Linked Insurance | 0 | Rs.75 |

Q. What is the current interest rate on EPF?

The current rate of interest is 8.75% p.a. The interest is compounded yearly.

The point to note in the interest calculation is done only on the part of EPF not on EPS. So if your contribution towards EPS is Rs.1,800 (12%) and your employer contribution towards EPF is Rs.550 (3.67%) and Rs. 1250 (8.67%) towards EPS, than the interest of 8.75% would be calculated on the amount of Rs.2,350.

Q. Which one is better – EPF Vs. PPF?

Employee Provident Fund is only for salaried person and Public Provident Fund is for self-employed person. But salaried person can enjoy benefit of both EPF as well as PPF while self-employed person can only take benefit of PPF.

| S.No. | Comparison Parameter | EPF | PPF |

| 1 | Who can Invest? | Only Salaried person. | Any Indian, except NRIs. |

| 2 | Quantum and Frequency of Investment | Statutory is 12% of basic +DA. Can voluntarily increase the contribution. Frequency is monthly from the salary itself. | Any Amount between Rs.500/- and Rs.1,50,000/- per year. A maximum of 12 contributions can be made per year subject to a minimum of Rs.100 per transaction. |

| 3 | Current Returns (w.e.f 1st April, 2015) | 8.75% p.a. | 8.70% p.a. |

| 4 | Loan Options | Partial Withdrawal. | Up to 50% of the balance of the 4th from the 6th year onwards. |

| 5 | Period of Investment | At the time of retirement or resignation, whichever is earlier. Can transfer account to new company till retirement. In case of death amount is paid to legal heirs. | Intially15 years which can be extended indefinitely by extending for 5 years each after that. In case of death amount is paid to legal heirs. |

| 6 | Tax Treatment at the time of investment as well as at the time of maturity | Contribution gets Section 80C benefit. Maturity is also tax free if contribution is withdrawn after completing 5 years of continuous service including transfers from different companies. Maximum Limit of Tax Benefit is the ceiling limit of Section 80C. | Contributed amount comes under Section 80C deduction. Maximum Limit of Tax Benefit is the ceiling limit of Section 80C. Maturity is also tax free. |

Unique aspect of PPF

The other unique feature of PPF is that in case of insolvency, the PPF account cannot be used to pay off debts in settlement process. However the PPF account can be utilized in case of Income Tax evasion.

Q. How to Check my EPF Balance Online?

There are two ways to check EPF balance online.

1. Register yourself at http://uanmembers.epfoservices.in/ and request for passbook. The passbook will be made available after 48 hours of request. This passbook will provide EPF account balance and contribution details made by you and your employer.

2. The second method to check EPF balance is via SMS. All you have to do is click on the link below: http://www.epfindia.com/site_en/KYEPFB.php

Select you PF office state and then your Regional PF Office. Enter your alpha numeric PF account number like RJ/UDR/123456/000/1234, your name and the mobile number on which you would like to get the EPG Balance Message. As soon as you hit the submit button, you would get the balance message on your mobile screen.

Q. How and when can I withdraw my EPF account money?

You can withdraw your EFP money for various reasons but only by fulfilling certain conditions, non-compliance of which would result in levying of penal interest.

Apart from the above stated conditions, if a person is taking a VRS at the age of 54 and above, then EPF money could be taken out only up to the 90% of the balance.

Q How Premature Withdrawal from EPF account is taxed?

Premature withdrawal means taking money out from the EPF account before 5 years of continuous service. Please note that continuous service means continuous contribution for 5 years. If you left the job after 3 years but made withdrawals after 5 years than also it would construed as premature withdrawal and full withdrawn amount would be taxed.

Budget 2015 has levied 10% TDS on premature withdrawal if exceeds Rs.30,000.

Q. What is Illegal Withdrawal of EPF Money?

As per EPF rules, withdrawing of EPF money at the time of switching jobs is illegal. You can withdraw only and only if you have not joined any other company within two months of quitting the job. You can transfer your EPF money once you get a new job.

Q. Can I contribute more than 12% towards EPF?

As per EPF Act, 1952, the minimum contribution of employee towards EPF account should be at least 12% but one can contribute up to 100% of your salary plus DA. This extra contribution from employee does is called VPF (Voluntarily Provident Fund) but remember this does not bound employer to contribute more. Employer can continue to contribute up to statutory limit of 12%.

However, many employers do not allow extra contribution of employee towards EPF. So you have to file an application with the Regional Provident Fund Commissioner.

Q. Is there any other benefit of EPF?

One more benefit of EPF account holder is that it gives a life insurance cover of Rs.60,000. This comes from the Employees Deposit Linked Insurance Scheme and for this employers have to contribute 0.50% of your monthly basic pay as premium for your life cover.

But companies that already provide life insurance benefits or group insurance policy to employees are exempted from contributing to this scheme.

Q. How to make any grievance of EPF?

Employees, who have failed to transfer their EPF balances when they switch jobs, or have applied for a transfer and have not got it, can use the EPF grievance system.

The easiest way to file a grievance is to do it online by visiting http://epfigms.gov.in/ portal.

To register a grievance, the complainant needs to click on the tab 'Register Grievance'. This tab opens a form that needs to be filled by the complainant, who has to select the category under which the complaint falls and describe the issue. Supporting documents can be uploaded to clarify the complaint.

Once the complaint form is filled by the applicant and submitted online, the complainant is allotted a unique registration number to track the status of his complaint. The complaint is scrutinized and if it is found valid, the same is forwarded to the relevant party for resolution.

Complaint tracking Complaint status can be tracked online and reminders can be sent using the registration number.

The other way to file grievance is to locate the regional office via http://search.epfoservices.org:81/locate_office/office_location.php?id=sm1_innerPage and drop the grievance by visiting the office

Best Tax Saver Mutual Funds or ELSS Mutual Funds for 2015

1. BNP Paribas Long Term Equity Fund

2. Axis Tax Saver Fund

3. IDFC Tax Advantage (ELSS) Fund

4. ICICI Prudential Long Term Equity Fund

5. Religare Tax Plan

6. Franklin India TaxShield

7. DSP BlackRock Tax Saver Fund

8. Birla Sun Life Tax Relief 96

9. Reliance Tax Saver (ELSS) Fund

10. HDFC TaxSaver

Invest Rs 1,50,000 and Save Tax under Section 80C. Get Good Returns by Investing in ELSS Mutual Funds Online

Invest in Tax Saver Mutual Funds Online

For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call

---------------------------------------------

Leave your comment with mail ID and we will answer them

OR

You can write to us at

PrajnaCapital [at] Gmail [dot] Com

OR

Leave a missed Call on 94 8300 8300