Download Tax Saving Mutual Fund Application Forms

Invest In Tax Saving Mutual Funds Online

Leave a missed Call on

94 8300 8300

Life Insurance Tax Corner| What are the tax benefits available to an individual in respect of premium paid on life insurance policies? | ||

| Life insurance premium paid by an individual qualifies for a deduction under Section 80C of Income Tax Act, 1961. An individual can claim deduction from gross total income on premium paid for a maximum of Rs 100,000 in each financial year. Amount deductible under Section 80C is equal to: | ||

| ||

| Certain investments and contributions have been specified as eligible ones for Section 80C. These investments/ contributions are eligible for deduction from gross total income. And a reduction in gross total income, leads to a reduction in the tax liability. Finally, the deduction limit for Section 80C has been pegged at Rs 100,000 per annum (pa). In other words, investors can make investments/contributions of upto Rs 100,000 every year and reduce their tax liability. | ||

| ||

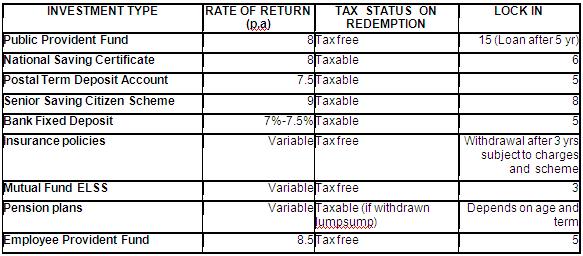

| Comparison of Various Tax Saving Instruments | ||

| ||

| What are the tax benefits available under pension plans? | ||

Premium paid towards a pension plan is eligible for a maximum benefit of Rs 100,000 under Section 80CCC. The said Section 80CCC limit falls under the overall Section 80C limit of Rs 100,000. In other words, the deduction aggregate, under Section 80C, 80CCC and 80CCD cannot exceed Rs 100,000. | ||

| Are maturity proceeds on life insurance and pension policies taxable? | ||

| The maturity proceeds of life insurance policies are not taxable. However, under pension plans, upto one-third of the maturity amount can be withdrawn in cash and the same is treated as tax-free. An annuity has to be purchased with the remaining two-third amount. Pension receipts from the same will be treated as income in the hands of the assessed and taxed accordingly. | ||

| Can tax benefits be claimed if the premium is paid by an individual on his/her spouse's policy? | ||

| Tax benefits can be claimed by an individual who pays life insurance premium on behalf of his/her spouse's policy under Section 80C of Income Tax Act, 1961. | ||

| If a person discontinues paying premium on his life insurance policy, does he get tax benefits? | ||

| If a person stops paying premium amounts on his/her life insurance policy, it amounts to discontinuation of the policy. Hence, he is not entitled to claim any tax benefits. | ||

| If a tax-payer discontinues the life insurance policy before premiums have been paid for a period of 2 years from the commencement of the policy, no tax deduction is allowed in respect of any premium paid on that policy in the year in which the policy is terminated. | ||

| Further, the amount of tax deduction, allowed for the premium paid in the preceding year, is treated as income and taxable for the year in which the policy is terminated. | ||

| If a person, investing in a Unit Linked Insurance Plan (ULIP), terminates his policy, can he claim any tax benefits on the same? | ||

| If a person participates in a Unit Linked Insurance Plan (ULIP) and then terminates his participation, he will not be entitled to claim any tax benefits. | ||

| What are the deductions available in respect of a medical insurance premium? | ||

| Medical insurance premium paid qualifies for deduction under Section 80D as follows: | ||

| ||

For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call

Leave a missed Call on 94 8300 8300

Leave your comment with mail ID and we will answer them

OR

You can write back to us at

PrajnaCapital [at] Gmail [dot] Com

---------------------------------------------

Invest Mutual Funds Online

Download Mutual Fund Application Forms from all AMCs

Download Mutual Any Fund Application Forms

---------------------------------------------

Best Performing Mutual Funds

- Largecap Funds Invest Online

- DSP BlackRock Top 100 Fund

- ICICI Prudential Focused Blue Chip Fund

- Franklin India Bluechip

- ICICI Prudential Top 100 Fund

B. Large and Midcap Funds Invest Online

- ICICI Prudential Dynamic Plan

- HDFC Top 200 Fund

- UTI Dividend Yield Fund

- Birla Sun Life Front Line Equity Fund

- Franklin India Prima

C. Mid and SmallCap Funds Invest Online

- Reliance Equity Opportunities Fund

- DSP BlackRock Small & Midcap Fund

- Sundaram Select Midcap

- IDFC Premier Equity Fund

- Birla Sun Life Dividend Yield Plus

- SBI Emerging Businesses Fund

- HDFC Mid-Cap Opportunities Fund

- ICICI Prudential Discovery Fund

D. Small and MicroCap Funds Invest Online

- DSP BlackRock MicroCap Fund

- Franklin India Smaller Companies

E. Sector Funds Invest Online

- Reliance Banking Fund

- Reliance Banking Fund

- ICICI Prudential Banking and Financial Services Fund

F. Tax Saver Mutual Funds Invest Online

1. ICICI Prudential Tax Plan

2. HDFC Taxsaver

- DSP BlackRock Tax Saver Fund

- Reliance Tax Saver (ELSS) Fund

G. Gold Mutual Funds Invest Online

- Relaince Gold Savings Fund

- ICICI Prudential Regular Gold Savings Fund

- HDFC Gold Fund

- Birla Sun Life Gold

H. International funds Invest Online

1. Birla Sun Life International Equity Plan A

2. DSP BlackRock US Flexible Equity

3. FT India Feeder Franklin US Opportunities

4. ICICI Prudential US Bluechip Equity

5. Motilal Oswal MOSt Shares NASDAQ-100 ETF