In our previous article, How have top Unit Linked Insurance Plan (ULIP) funds performed in the last 5 years: Part 1, we have seen how the top equity oriented ULIP funds have performed in the last 5 years. We had seen the performance of the ULIP funds over the last 5 years has almost been at par with mutual funds performance, for some categories of ULIP equity funds. However, the actual returns to the investors will be lower than the gross returns from the ULIP funds, due to various ULIP charges like Premium allocation charge, Policy administration charge and Mortality charge. To understand how these charges affect ULIP returns, please refer to our article, Demystifying Unit Linked Insurance Plan (ULIP) Charges and Returns. A big portion of these charges are front loaded, so returns improve in the middle and later part of the policy term. In this article, we will see how top balanced and debt oriented ULIP funds have performed in the last 5 years.

Balanced ULIP fund – High Equity allocation

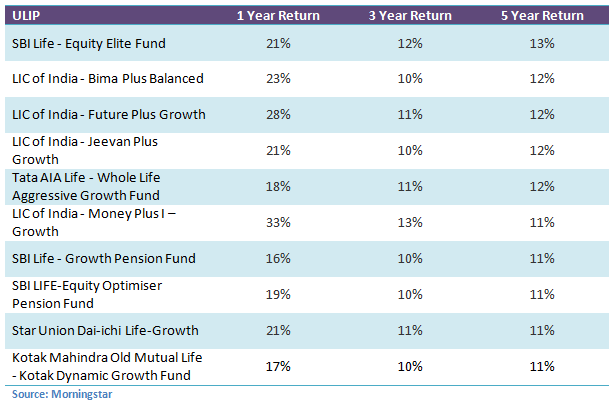

ULIP funds belonging to the balanced fund category with high equity allocation have given 5 years annualized returns of 10.2% at the category level. Compared to top performing balanced mutual funds, the returns are much lower. The top 5 ULIP funds in this category have given annualized returns of 12 – 13% over the last 5 years. The table below lists the top 10 Balanced ULIP funds with high equity allocation (individual policies only) based on 5 years annualized returns (3 and 5 year returns are annualized).

We can see that the top 10 balanced ULIP funds with high equity allocation have given 11 – 13% returns in the last five years. The top 10 list is dominated by ULIPs from LIC. The last one year returns of some of the LIC balanced ULIP funds have been quite good. However, investors need to see, if this performance can be sustained in the future.

Balanced ULIP fund – Moderate Equity allocation

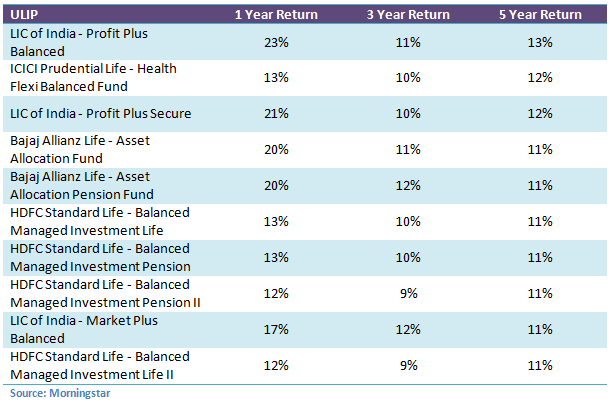

ULIP funds belonging to the balanced fund category with moderate equity allocation have given 5 years annualized returns of 9.3% at the category level. The top 5 ULIP funds in this category have given annualized returns of 11 – 13% over the last 5 years. The table below lists the top 10 Balanced ULIP funds with moderate equity allocation (individual policies only) based on 5 years annualized returns (3 and 5 year returns are annualized).

We can see that the top 10 balanced ULIP funds with moderate equity allocation have given 9 – 12% returns in the last five years. The top 10 list is dominated by ULIPs from LIC, Bajaj Allianz and HDFC Standard Life. The last one year returns of some of the LIC and Bajaj Allianz balanced ULIP funds with moderate equity allocations have been quite good. However, investors need to see, if their performance can be sustained in the future.

Balanced ULIP fund – High Debt allocation

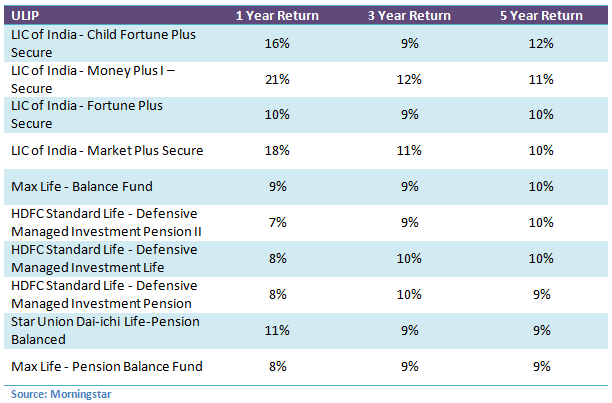

ULIP funds belonging to the balanced fund category with high debt allocation have given 5 years annualized returns of 8.3% at the category level. Compared to top performing balanced mutual funds with high debt allocation, the returns are almost on par. The top 5 ULIP funds in this category have given annualized returns of 10 – 12% over the last 5 years. The table below lists the top 10 Balanced ULIP funds with high debt allocation (individual policies only) based on 5 years annualized returns (3 and 5 year returns are annualized).

We can see that the top 10 balanced ULIP funds with high equity allocation have given 9 – 12% returns in the last five years. The top 10 list is dominated by ULIPs from LIC. The last one year returns of some the LIC balanced ULIP funds with high debt allocations have been quite good. However, we need to see, if this performance can be sustained in the future.

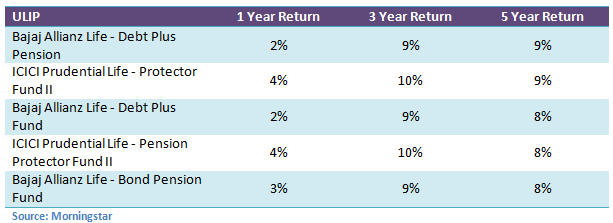

Medium term ULIP Debt Fund

These are ULIP debt funds where the underlying bond portfolio has an effective duration of 3 – 10 years. These funds have given average 5 year annualized return of 7% at the category level. The top 5 funds in this category have given 8 – 9% returns. The table below lists the top 5 medium term ULIP debt fund (individual policies only) based on 5 years annualized returns (3 and 5 year returns are annualized).

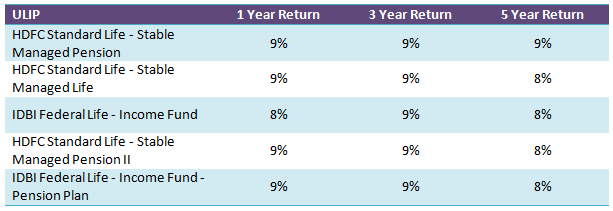

Short term ULIP Debt Fund

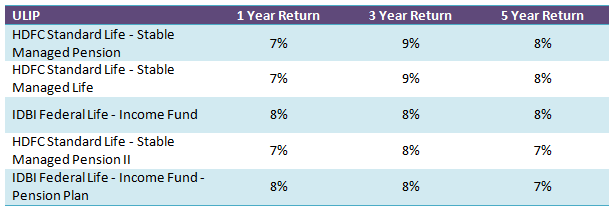

These are ULIP debt funds where the underlying bond portfolio has an effective duration of 1 – 3 years. These funds have given average 5 year annualized return of 7% at the category level. The top 5 funds in this category have given 8 – 9% returns. The table below lists the top 5 short term ULIP debt fund (individual policies only) based on 5 years annualized returns (3 and 5 year returns are annualized).

Ultra Short term ULIP Debt Fund

These are ULIP debt funds where the underlying bond portfolio has an effective duration of less than 1 year. These funds have given average 5 year annualized return of 8% at the category level. The top 5 funds in this category have given 8 – 9% returns. The table below lists the top 5 ultra short term ULIP debt fund (individual policies only) based on 5 years annualized returns (3 and 5 year returns are annualized).

Conclusion

In this two part series, we have seen how the top ULIP funds for various categories have performed in the last 5 years. How will you identify a ULIP that will give great returns? It is extremely difficult. The return for every ULIP policy will be different due to the charges. Therefore, if you want to invest in ULIPs, you should consult with Prajna Capital with considerable experience in ULIPs to help you identify the plans that will help you meet your life insurance and investment objectives.

Top 10 Tax Saving Mutual Funds to invest in India for 2016

Best 10 ELSS Mutual Funds in india for 2016

1. BNP Paribas Long Term Equity Fund

2. Axis Tax Saver Fund

3. Franklin India TaxShield

4. ICICI Prudential Long Term Equity Fund

5. IDFC Tax Advantage (ELSS) Fund

6. Birla Sun Life Tax Relief 96

7. DSP BlackRock Tax Saver Fund

8. Reliance Tax Saver (ELSS) Fund

9. Religare Tax Plan

10. Birla Sun Life Tax Plan

Invest in Best Performing 2016 Tax Saver Mutual Funds Online

For further information contact Prajna Capital on 94 8300 8300 by leaving a missed call

---------------------------------------------

Leave your comment with mail ID and we will answer them

OR

You can write to us at

PrajnaCapital [at] Gmail [dot] Com

OR

Leave a missed Call on 94 8300 8300

-----------------------------------------------